What Should Kids Know About Credit, Why, and at What Age?

The trick to teaching credit is finding the balance between what a kid needs to know and what they’re capable of grasping based on age and grade level.

A recent national study done by FICO shows that the generations who feel most secure in their finances are those that completely or somewhat understand credit scores.

But if students can’t yet hold a job or open a credit card, how can they master concepts like FICO® Scores and interest without hands-on experience before graduation? By simulating real-world scenarios, we allow students to learn by doing while trading real-life consequences for in-game trial and error, building a credit-confident generation.

The Invisible Score: What Today’s Students Actually Know?

According to the FICO study, “one in five” students and young adults (ages 14 - 29) say they “understand credit scores a little or not at all,” and “29% said they either do not have a credit score or do not know if they have one.” The knowledge gap becomes obvious when compared with older adults (ages 62 to 80), where only 8% report something similar.

So, What Should Students Understand About Credit and When?

By graduation, students should understand that credit is essentially borrowed money—whether via loans, mortgages, or credit cards. They should also understand the makeup of a credit report and how a FICO® Score is calculated:

- Payment history: 35%

- Outstanding debt: 30%

- Credit history length: 15%

- Credit mix: 10%

- Pursuit of new credit: 10%

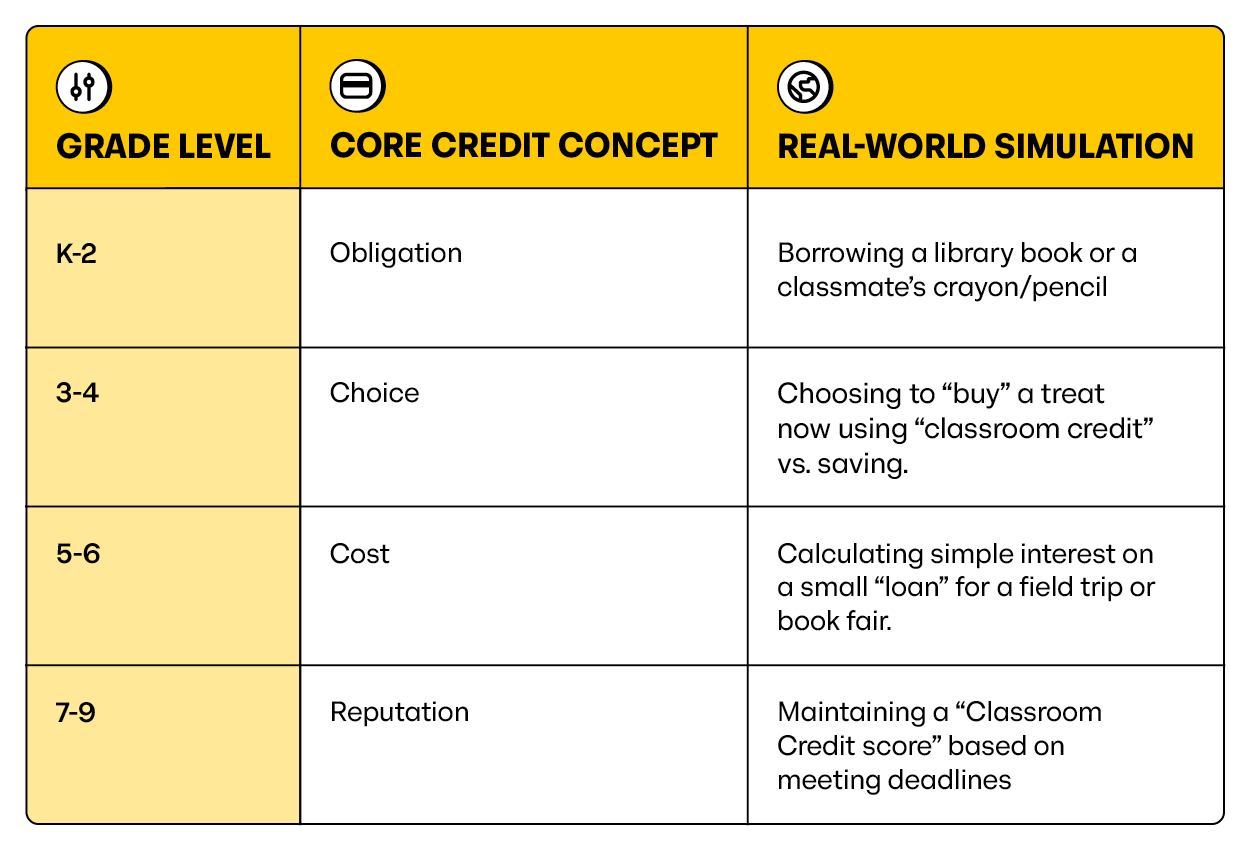

Ideally, credit education should be broken down by age:

While you can dive into your state’s specific requirements on Banzai’s standards alignment page, we’ve provided a general overview below of what students should know at every grade level.

Lower Elementary (Grades K–2): The Foundations of Credit

Younger students may not be ready for all the complexities of credit and its effects on financial health. At this age, the goal is to distinguish between "mine" and "yours" and understand the obligation of a loan. If a student learns the following principals, they are already miles ahead of those who haven’t gotten the opportunity to learn about credit at all.

- Borrowing vs. Gifting: Understanding that a "gift" is yours to keep, while something "borrowed" (whether a toy or a dollar) must be returned.

- The Concept of Trust: Learning that if you don't return what you borrowed, people may not lend to you again (the "pre-credit score" lesson).

- Payment Methods: Identifying that people use different things to pay for goods (coins, bills, and "plastic cards").

Upper Elementary (Grades 3–5): Digital Credit

This is where the curriculum bridges the gap between physical money and 'invisible' digital credit. At this stage, students learn there is much more than meets the eye when an adult uses a seemingly 'magical' card to pay for everyday things.

- Credit vs. Debit: Understanding that a debit card takes money you already have, while a credit card isn’t your money and you have to pay it back.

- Interest as a Cost: Introducing the idea that borrowing money isn't free. If you borrow $10 today, you might have to pay back $11 later.

- Opportunity Cost: Understanding that if you use credit to buy something now, you are "spending" your future income, which means you can't buy something else later.

- Reliability & Reputation: Discussing how a person's history of paying (or not paying) back loans affects their ability to borrow in the future.

Middle School (Grades 6–8): Credit History

In Middle School, a good focus shift is to Credit History. Students learn that their financial actions create a "trail" that follows them and is “graded” accordingly:

- The Components of Credit History: Identifying what goes into a credit report (payment history, amount owed, and type of debt).

- Types of Debt: Distinguishing between secured (car loan) and unsecured (credit card) debt.

- Interest: Understanding that interest is the "rent" you pay to use someone else’s money.

- Identity Theft Basics: Learning how personal information (SSN, birthdays) is used to commit credit fraud and the concept of "phishing."

By eighth grade, students should be able to calculate how much a small loan costs over time using simple interest, identify the consequences of not paying a bill on time (late fees + damage to reputation), and decide when it’s smarter to use cash versus a debit card or a "buy now, pay later" service.

High School (Grades 9–12): Advanced Credit Concepts

In high school, the curriculum becomes more technical. This is where understanding Credit History turns into learning about the FICO® Score—used by 90% of top lenders in the US. This is when actual financial math is applied.

The FICO Formula: Understanding the weighted factors of a FICO® Score:

- 35% Payment History

- 30% Outstanding Debt (Amounts Owed)

- 15% Credit History Length

- 10% Credit Mix

- 10% Pursuit of New Credit

APR (Annual Percentage Rate): Understanding that APR includes both interest and fees, making it the true "price tag" of a loan.

Rights and Disputing: Knowing the Fair Credit Reporting Act—specifically how to get a free credit report and the process for disputing errors.

Bankruptcy & Long-term Debt: The legal and 10-year financial consequences of declaring bankruptcy.

By graduation, students should be able to: read and analyze a sample report to find errors or "red flag" accounts and understand and shop for different loans using APR as a comparison tool (student loan shopping is a good way to practice this). They should also be able to calculate how many years it takes to pay off a balance if you only pay the minimum and calculate whether a specific salary can realistically support a specific monthly loan payment.

Note: Banzai recently partnered with FICO to integrate FICO® Score A Better Future Fundamentals directly into their simulations.

SOURCE:

FICO, 2023. "Consumer Survey Reveals Key Relationship between Financial Confidence and Credit Scores," FICO Newsroom, Fair Isaac Corporation, January 26.